These changes for Tier 1 and Tier 2 for-profit entities apply to annual periods beginning on or after 1 January 2024, so already apply to entities preparing 30 June 2024 half-year financial statements.

In addition, Tier 1 entities preparing 30 June 2024 annual financial statements must disclose the effect of these amendments on the classification of liabilities as required by NZ IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors, paragraph 30. This includes describing and quantifying the impact in your 30 June 2024 financial statements because comparatives will have to be restated.

Classifying your liabilities may be impacted by one or more of the changes to NZ IAS 1 Presentation of Financial Statements, namely:

- The right to defer settlement need not be unconditional and must exist at the end of the reporting period

- Classification is based on rights to defer, not intention

- Early conversion options for convertible notes that can be settled before maturity by issuing the entity’s own equity instruments will result in the underlying liability being classified as CURRENT if the conversion feature is classified as a liability/derivative liability rather than as equity.

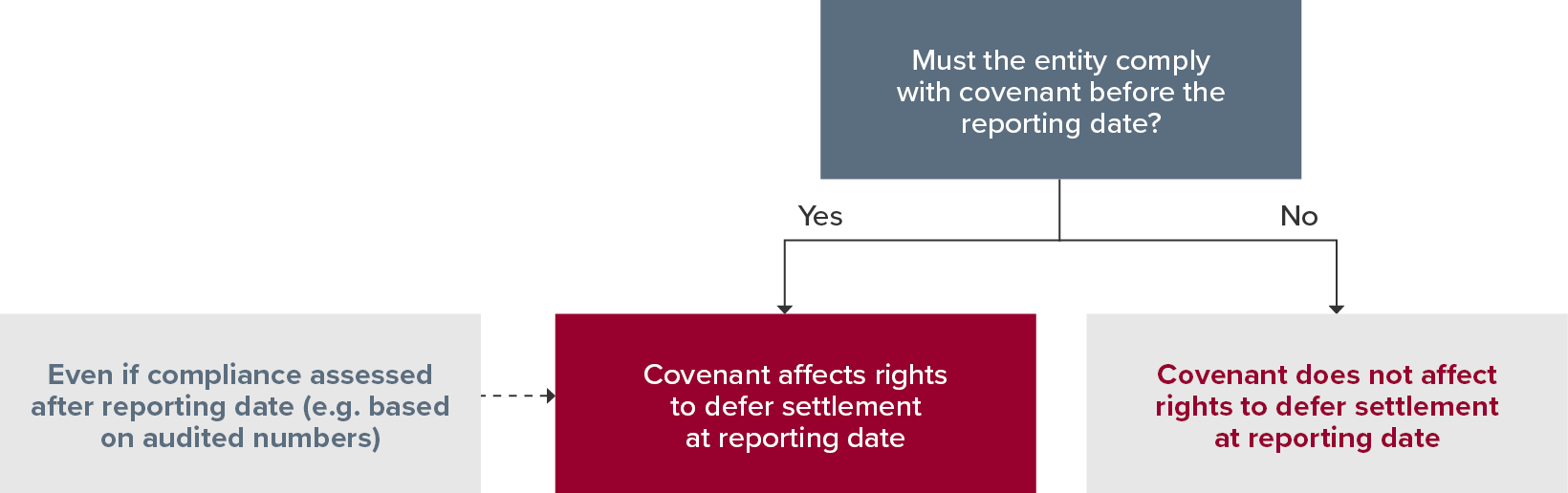

Regarding 1., if your entity has loan arrangements subject to covenants, the amendments clarify when the covenants affect classification at the reporting date. This is illustrated in the diagram below.

Assessing whether the entity must comply with a loan covenant before the reporting date may depend upon whether bankers have provided a ‘waiver’ or a ‘period of grace’. Our publication uses a flowchart and examples to help you determine the correct classification of your loan arrangements.